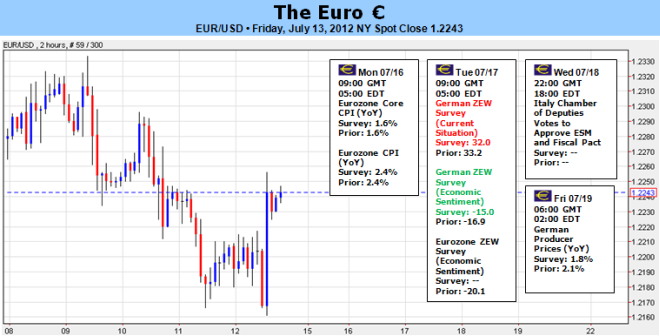

Euro at historical midpoint needs collapse in risk appetite to proceed

14 July 2012 03: 00 GMT

fundamental Outlook for the euro: neutral

fundamental Outlook for the euro: neutral

fundamental Outlook for the euro: neutral

There is no shortage of basic

justification for the euro to expand its painful collapse, but history has

taught us that the market will decide, it is important and what is not. Last

week, EURUSD fell to its lowest level in two years - a region that is intended

for historical area (about 1.2135) especially in the middle between the two.

Purely fundamental point of view, we could show the failed promises of the EU

Summit and erosion of confidence in the ability to stabilize its financial

sector as the source for this plight. But the headlines were not line, until the

news crossing the wires more sparsely (compared to the lead up to the Summit two

weeks ago) and price action. By the last week of the EURUSD daily far the S

& P 500 futures than one organized event drivers.

In the past the correlation between the became world's most liquid currency

pair (EURUSD) and my preferred measure of risk appetite (the course long biased

and stimulus-based S & P 500) quite heavily. This should in no small part

the greenback as the ultimate liquidity provider and the euro position as Center

of the world's largest financial threat. However the balance of emotions leads

around moving forward rather the health of the European financial system, rather

than the other way. This means that the round of open and detail-deficient buy

vows of the EU Summit as an another successful bid will be on time - rather than

to solve the underlying problem.

In General, can risk trends, we measure the

market tolerance for the inclusion of otherwise dubious European assets. EURUSD

position just above its historical center and the ground of a long-term

technical congestion pattern specified, it makes sense that a strong fundamental

impetus is necessary if we are to finally move below 1.2000. Looking for heavy

hitting catalysts ahead, there mangelnder are big-ticket items such as a

provisional GDP reading to global growth expectations or a critical policy

collection, which could on the initiative hopes to lead. The market remains open

to distract his own way without distractions or catalysts to it to find. We have

a barrel on Monday to IMF sees growth. There is some ongoing hope that Bernanke

the topic QE3 Tuesday and Wednesday - another source of disappointment can to

respond to testimony his Congressional, if it does not occur to one. Perhaps one

of the most influential (but derogatory vague) developments is the construction

of the 2Q U.S. corporate earnings season. To impress that collective

expectations for returns have been set too high chance of the market is an open

invitation to the relax.

Although the general condition of the atmosphere on global markets should not

more influence over the euro next week can have health, we optimize the

fundamental event risk of the euro process list. Given the dubious, long-term

health of the eurozone itself; Undermine developments that gain the offer of

stability shifts in the global currents can expose further troubling the region.

Perhaps the most compelling event risk is EU Finance Ministers meeting on

Friday. This is supposedly a follow up of the July 9 meeting the implementation

of direct rescue of the ruler of the ESM, to discuss terms Spain rescue and

again Greece. After two details to work out failed in the Tower, yet

expectations probably low. On Wednesday, the EU will release a report on the

public finances of the euro zone. This can provide either a rude awakening or

(more likely) it an optimistic turn on bad numbers - leading sets in the market

write. Also worth mentioning is a round of bond auctions. Greece, Portugal (his

second since code format order the market since his rescue), Spain and Italy to

sell all debt. Even though they have no serious market events be on the move,

they have constantly pursued, deteriorated confidence.

As we weigh the

fundamental reality to the capricious appetite of speculators, it is considering

alternative complications in capital flows. A theory for the euro, which has

gained considerable traction recently is that a deterioration leads the regional

financial conditions and decrease of your risk tolerance, capital of foreign

investors to repatriate European banks. A Bank of America research report

illustrates a more foreign euro banks as a 40 percent decline in stocks since

2008. This could prove that a permanent buffer with the sale of pressure

thought, completely probably would compensate for it not. Now I'm a basic bear

with technical and speculative reservations for follow through. -JK

DailyFX provides Forex News and technical analysis on the latest trends

affecting the global foreign exchange markets.

Learn forex trading with a

free practice account and trading charts of FXCM.

14 July 2012 03: 00 GMT

No comments:

Post a Comment