Fundamental Outlook for US-dollar: bullish

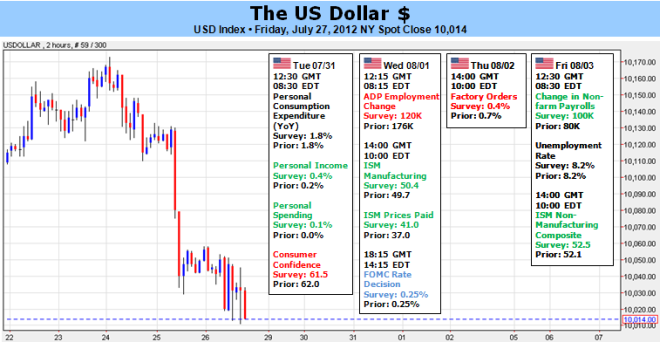

The Dow Jones FXCM dollar index (ticker: USDOLLAR) ended the week slightly lower on a sharp late week selloff, but earlier signs of life suggest that the dollar remains comfortably within its upward trend and to win in the coming weeks.

The US dollar open market Committee of the current tariff rallied strongly after the much-anticipated release of minutes from the US Federal decision, but a sharp Friday sale leaves the greenback slightly lower next week trading launched. A relatively limited schedule of economic event risk probably signals that the USD continues to trade from larger financial market sentiment. This is true in particular for the Australian dollar / US dollar pair and other commodity-linked currencies as $correlations to S P 500 & trade close to record strength. So higher specialized works will depend whether the dollar almost certainly of stock indices and other financial market sentiment the trajectory. Two important issues on international investors heads are pretty clear: the future of the US Federal Reserve quantitative easing (QE) and the current European fiscal and financial crises.

On the home front, USD bulls reacted positively to signs that the Fed struck a cautious note over the possibility of more QE in recent FOMC minutes. Greenback weakened considerably by 2009 on the first wave of QE and markets exactly QE2 expected in 2010 decreased. Give the US currency could back some of its recent gains on the future announcement of QE3. Still, the Fed stressed the caution that the next wave is a done deal, and the dollar could remain strong, as the Fed keeps the line on the further expansion of the balance sheet. To force across the Atlantic European fiscal and financial crises continue to significant financial market turbulence and greater risk appetite could be depressed about foreseeable. Credit rating agency of Moody's was to pour the latest gasoline in the fire, as it downgraded sovereign credit rating of Italy. The move itself was not surprising, but the timing of the downs seemed to catch many traders off guard. Italian Government, that 10-year quickly traded in towards the top of their several months reach responds yields as traders on the message. (Bond yields above, if the prices go down)

Instability in the third and fourth largest economies of the eurozone (Italy and Spain, respectively) is probably the most immediate threat to the euro as a currency. We keep a watchful eye on Italian and Spanish Government - returns since Spain is a 10-year craft dangerously close to the ultimate 7 percent in Friday of close. The safe harbor U.S. dollar is accordingly flare-ups in the European market will benefit from any tensions. The last sale starts in Italian and Spanish bonds (increase in income) stress that markets tense despite the recently presented Spanish bailout and others remain growth-oriented European action. Continuing turbulence favoured remaining long 'security' and short 'risk' - long US dollar and short euro.

Our shorter-term bias is clear, and we believe that the recent outbreak of the U.S. dollar may be only the beginning of a larger rally. However, much of dollar Outlook depends on whether S & P keeps the US 500 critical support levels. A breakdown of the financial risk of market sentiment would likely produce the US dollar rally what we have expected that. -DR

EUR/USD didn't move much following the better than expected investor optimism survey. After the close of a bearish month that saw a 7% decline for the euro against the dollar, the pair started June with a bounce back above 1.2400 from a fresh 2-year low below 1.2300 during Friday's trading.

EUR/USD didn't move much following the better than expected investor optimism survey. After the close of a bearish month that saw a 7% decline for the euro against the dollar, the pair started June with a bounce back above 1.2400 from a fresh 2-year low below 1.2300 during Friday's trading. A look at the encompassing structure sees the EURUSD trading within the confines of a broad descending channel formation dating back to the August highs with the single currency rebounding off channel resistance of an embedded channel dating back to the February highs. Key daily resistance stands at the 1.33 figure with a breach above this level challenging the 1.34-figure and the February highs at 1.3485. Daily support rests with the 100-day moving average at 1.3115 and the 1.30-figure.

A look at the encompassing structure sees the EURUSD trading within the confines of a broad descending channel formation dating back to the August highs with the single currency rebounding off channel resistance of an embedded channel dating back to the February highs. Key daily resistance stands at the 1.33 figure with a breach above this level challenging the 1.34-figure and the February highs at 1.3485. Daily support rests with the 100-day moving average at 1.3115 and the 1.30-figure.  The scalp charts shows somewhat of a mixed outlook for the EURUSD. Clear bearish divergence in the relative strength index alluded to the euro’s decline today with the single currency rebounding off the 38.2% Fibonacci extension taken from the March 27th and May 1st crests at 1.3130 before encountering soft resistance at 1.3165. Subsequent resistance levels are eyed at the 23.6% extension at 1.3190 backed by 1.3210, 1.3240 and 1.3260. A breach above the May 1st high at 1.3280 negates this specific setup with such a scenario eyeing targets above the 1.33-handle. Interim support rests with the 38.2% extension with support targets seen lower at 1.3110, the 50% extension at 1.3085 and 1.3060. The initial objective remains the 1.30 figure which has been met with sharp rebounds over the past three months each time the level has been tested. Should the print prompt a bearish response look to target downside levels with a break below the 1.30-threshold offering further conviction on our directional bias.

The scalp charts shows somewhat of a mixed outlook for the EURUSD. Clear bearish divergence in the relative strength index alluded to the euro’s decline today with the single currency rebounding off the 38.2% Fibonacci extension taken from the March 27th and May 1st crests at 1.3130 before encountering soft resistance at 1.3165. Subsequent resistance levels are eyed at the 23.6% extension at 1.3190 backed by 1.3210, 1.3240 and 1.3260. A breach above the May 1st high at 1.3280 negates this specific setup with such a scenario eyeing targets above the 1.33-handle. Interim support rests with the 38.2% extension with support targets seen lower at 1.3110, the 50% extension at 1.3085 and 1.3060. The initial objective remains the 1.30 figure which has been met with sharp rebounds over the past three months each time the level has been tested. Should the print prompt a bearish response look to target downside levels with a break below the 1.30-threshold offering further conviction on our directional bias.  As expected, the European Central Bank struck a cautious outlook for the region after keeping the benchmark interest rate at 1.00%, while central bank President Mario Draghi argued that ‘any exit strategy talk for the time being is premature’ as the region faces a double-dip recession. The dovish tone held by the ECB dragged on the Euro, with the EURUSD falling back towards the 1.3100 figure, but we saw the single currency consolidate during the North America trade to end the day at 1.3140.

As expected, the European Central Bank struck a cautious outlook for the region after keeping the benchmark interest rate at 1.00%, while central bank President Mario Draghi argued that ‘any exit strategy talk for the time being is premature’ as the region faces a double-dip recession. The dovish tone held by the ECB dragged on the Euro, with the EURUSD falling back towards the 1.3100 figure, but we saw the single currency consolidate during the North America trade to end the day at 1.3140.