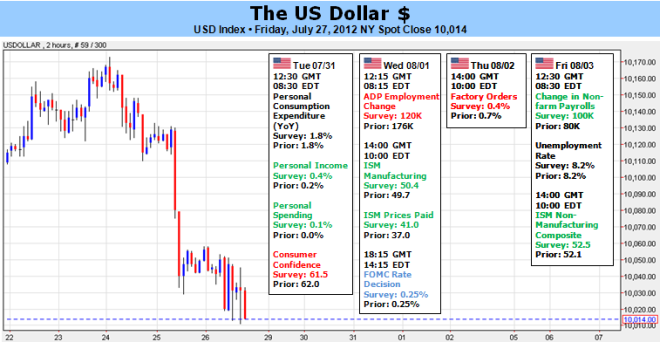

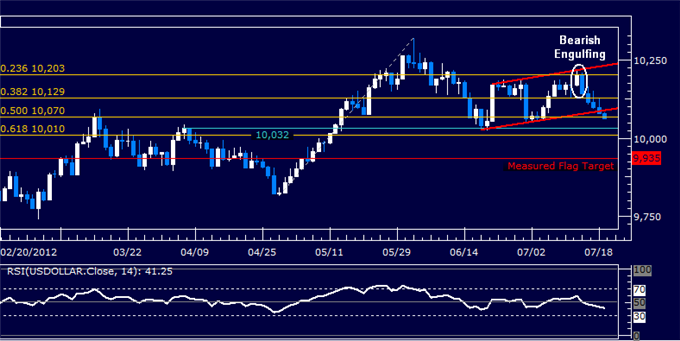

Dollar Ready to Rally after NFPs Disappoint, Reality Setting In Euro Down Sharply Against Safe Havens and Carry Currencies this Week British Pound As Exposed as Ever, BoE Stimulus Merely Waters Currency Down Japanese Yen: JGBs Close at Recent Historical Low, Stimulus Ahead? Canadian Dollar Offers Limited Labor Data Reaction, Don’t Write Off Late Reaction Swiss Franc Fight Growing Costly for SNB According to Reserves Update Gold: In the Absence of Balance Sheet Growth, Dollar is a Better Safe Haven Dollar Ready to Rally after NFPs Disappoint, Reality Setting In

Since peaking at 21-month highs back at the beginning of June, the US Dollar has struggled to regain traction. Then again, currency has withstood a general risk appetite run that has otherwise lifted equities and other growth-linked assets to two-month highs. This resistance taps into the underlying fundamental current that has defined a tangible deterioration in growth and yield expectations to be further supplemented by a sense of hope. A rational assessment of ‘risk’ and ‘reward’ for these markets offers a very discouraging picture of the investment landscape. For potential return, the aggregate yield of the major currencies’ 10-year government notes (Treasuries are arguably the foundation for all rates of return) is just off of the record low set back in June. Furthermore, it is fully 38 percent lower than the low-point back in 2009 (in the aftermath of the worst crisis in modern history and the massive stimulus effort that follows). The only reprieve in the standard equilibrium is that volatility readings are still exceptionally low and set lower peaks when they do swell – perhaps the greatest effect stimulus has had.

Restraint on volatility (risk) does not translate into a strong position to foster risk trends. Given the exceptionally low levels of return in the market, it wouldn’t take much to scare the holdouts from their positions. So what has kept sentiment buoyant and the dollar under pressure? Hope. Hope that central bankers or lawmakers would take advantage of critical policy gatherings to expand their support of the system – or at the very least inject capital into the system to provide a temporary high. Yet, the Greek election, Fed rate decision, EU Summit and ECB rate decision have one after the other fallen short of the type of stimulus that speculators have grown addicted to. Moving forward, the docket critically lacks the kind of events that the market would typically peg as opportunities for officials to announce more support. If that is the case, enduring bulls will have to seriously evaluate the soundness of their positions. Readings like the disappointing NFPs release this past Friday will carry greater weight. In the upcoming week, we should watch specifically for the Chinese 2Q GDP reading and start of US 2Q earnings season.

Euro Down Sharply Against Safe Havens and Carry Currencies this Week

Little more than a week ago, a number of Euro Zone officials were trumpeting the success in the EU Summit’s compromise towards passing agendas that had received tremendous debate but gained little practical traction in the preceding months. The euro wasn’t immune to the exuberance as the currency won its biggest single-day rally since October 27. However, we made the technical and fundamental connection to that previous rally as a Greek restructuring that did little to solve the region’s underlying problems and the EURUSD’s subsequent, multi-week tumble immediately after the rally. The Summit’s vows (a common bank overseer, dropping seniority on Spanish bailout funds, directly funding banks using the ESM and allowing the ESM to purchase government bonds) are so far still promises without action. We’ve been here many times before with European programs that merely buy time rather than solve problems, and it has made this market skeptical. The ECB assured that stimulus hopes would be further flushed (and cut the currency’s yield to boot). That left us open to the a dose of reality Friday that banks were closing European money market funds (removing havens for liquidity in rough seas), Spanish yields climbed back up to 7 percent and Greece announced it was dropping its bid for easier conditions on its second bailout. On Monday, the ESM is expected to begin operation and Finance Ministers are expected to meet; but given the EURUSD’s two-year low, it seems the market doesn’t seem much potential.

British Pound As Exposed as Ever, BoE Stimulus Merely Waters Currency Down

Various Bank of England officials have repeatedly warned that the Euro Zone crisis poses the greatest threat to the UK’s financial and economic health. These warnings are starting to gain more traction amongst pound traders. This past week’s decision to lift the bond purchasing program by 50 billion sterling was a move directed at bolstering growth and shoring markets in the event of a crisis spread; but if EU situation did prove infectious, those efforts would matter little. To truly prevent a crisis in Great Britain, the Euro Zone must be stabilized. And that looks unlikely.

Japanese Yen: JGBs Close at Recent Historical Low, Stimulus Ahead?

The benchmark 10-year JGB (Japanese Government Bond) yield dropped Friday to close at its lowest level (0.80 percent) on record. We could label this a safe haven move by the markets (as people pull funds into the world’s second largest economy) or a natural side effect of capital repatriation by Japanese investors. However, there is also a meaningful sense of stimulus forecast in this move. Next week, we have the BoJ rate decision on Friday. Over the past weeks, central banks have eased (the ECB took deposit rates to zero), setting the stage for Japan.

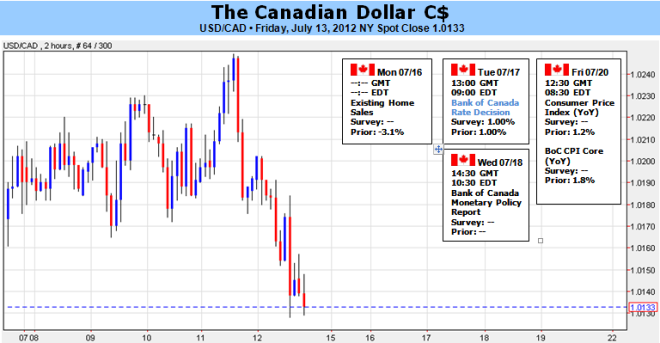

Canadian Dollar Offers Limited Labor Data Reaction, Don’t Write Off Late Reaction

Though the headline employment change number wasn’t as extraordinary as some of the readings earlier this year, the June data was nevertheless solidly bullish. The 7,300 person increase in payrolls marks the fourth consecutive increase and was backed by a 29,300 net increase in full-time positions. Furthermore, wage growth accelerated to a near, three-year high. The loonie’s hold up was its relationship to the US fundamental backdrop. That said, Canada is truly standing out for its relative financial health – a boon against fellow high yielders like AUD.

Swiss Franc Fight Growing Costly for SNB According to Reserves Update

We have known that the SNB’s effort to stem the franc tie hasn’t been going very well – not difficult to interpret given the EURCHF’s refusal to rise from 1.2000. Yet, nothing puts the situation into better perspective than seeing the amount of funds put into the effort. The central bank released its May FX reserves. Is the 20 percent increase over the month to a record 365 billion francs enough to encourage a fresh policy approach? Buying an unlimited amount of euros as a regional crisis intensifies hardly seems a viable strategy.

Gold: In the Absence of Balance Sheet Growth, Dollar is a Better Safe Haven

Gold is an ideal alternative to currencies and safe haven government bonds that are otherwise manipulated by their respective monetary authorities. So then why hasn’t gold gained these past weeks with Operation Twist 2, the PBoC rate cut, ECB rate cut and EU Summit vows? These are certainly efforts to ease, but they don’t bolster balance sheets. Furthermore, there is the lingering issue of liquidity.

For Real Time Forex News, visit: http://www.dailyfx.com/real_time_news/

**For a full list of upcoming event risk and past releases, go to www.dailyfx.com/calendar

ECONOMIC DATA

Next 24 Hours

Early business activity measures.

JPY Current Account Total (Yen)

The forecasted trade deficit for May is expected to tip the third biggest shortfall on record.

JPY Adjusted Current Account Total (Yen)

JPY Trade Balance - BOP Basis (Yen)

JPY Current Account Balance (YoY)

CNY Consumer Price Index (YoY)

Easing inflation could help guide the stimulus to austerity balance.

CNY Producer Price Index (YoY)

Hit a near, three-year high last month.

JPY Eco Watchers Survey: Current

Business activity indicators that reflect on a volatile economic situation.

JPY Eco Watchers Survey: Outlook

A slip in the jobless rate will do nothing more than make the franc a slightly better safe haven.

Trade is one of the primary reasons Germany fights so adamantly to retain the euro and EMU.

EUR German Current Account (euros)

EUR German Trade Balance (euros)

EUR Euro-Zone Sentix Investor Confidence

Critical confidence measure for a troubled region.

CAD Business Outlook Future Sales

Rarely market moving but important measures to confirm financial stability

CAD Bank of Canda Senior Loan Officer Survey

With wages and employment stagnating, consumer spending depends on credit.

Euro Area Fin Mins Meet in Brussels

Alcoa First Bluechip to Report 2Q Earnings

USD Fed's Evans Speaks in Thailand

USD Fed's Williams Speaks in Idaho

SUPPORT AND RESISTANCE LEVELS

To see updated SUPPORT AND RESISTANCE LEVELS for the Majors, visit Technical Analysis Portal

To see updated PIVOT POINT LEVELS for the Majors and Crosses, visit our Pivot Point Table

CLASSIC SUPPORT AND RESISTANCE –EMERGING MARKETS 18:00 GMTSCANDIES CURRENCIES 18:00 GMT

INTRA-DAY PROBABILITY BANDS 18:00 GMT

Dow Jones FXCM US Dollar Index - Daily Chart - Created Using FXCM Marketscope

2.0

Dow Jones FXCM US Dollar Index - Daily Chart - Created Using FXCM Marketscope

2.0

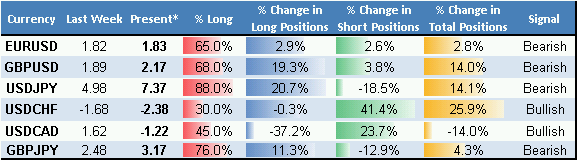

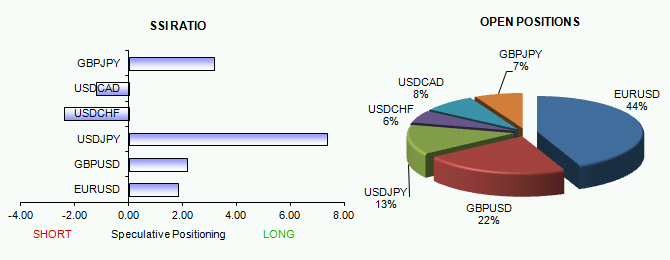

retail forex trading crowds have aggressively sold into US dollar (ticker:

USDOLLAR) rallies against the euro and British pound. Such one-sided sentiment

gives contrarian signal that the EURUSD and GBPUSD may fall to fresh lows.

retail forex trading crowds have aggressively sold into US dollar (ticker:

USDOLLAR) rallies against the euro and British pound. Such one-sided sentiment

gives contrarian signal that the EURUSD and GBPUSD may fall to fresh lows.

Graph created with the scope of the market - prepared by Chen Wen - Tzu

Graph created with the scope of the market - prepared by Chen Wen - Tzu Dow Jones FXCM Dollar Index (lhs)

Dow Jones FXCM Dollar Index (lhs)

Daily Chart - Created Using FXCM Marketscope 2.0

Daily Chart - Created Using FXCM Marketscope 2.0  Daily Chart - Created Using FXCM Marketscope 2.0

Daily Chart - Created Using FXCM Marketscope 2.0  Daily Chart - Created Using FXCM Marketscope 2.0

Daily Chart - Created Using FXCM Marketscope 2.0

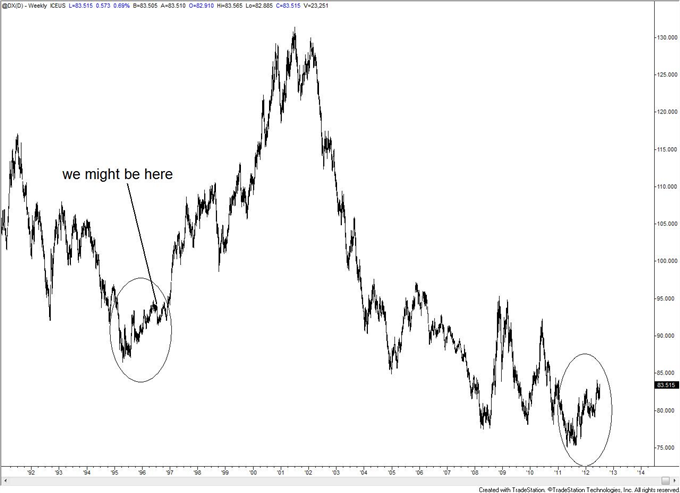

US DOLLAR INDEX:The market has now taken out some major resistance by 10,100 to open the door for fresh upside and a bullish continuation over the coming weeks. Next key resistance comes in by the 10,500 area, although, with daily studies now overbought, look for opportunities to buy on dips back towards 10,000 where a fresh higher low is now sought out.

US DOLLAR INDEX:The market has now taken out some major resistance by 10,100 to open the door for fresh upside and a bullish continuation over the coming weeks. Next key resistance comes in by the 10,500 area, although, with daily studies now overbought, look for opportunities to buy on dips back towards 10,000 where a fresh higher low is now sought out.